In my house, there's one thing that's never missing from the fridge:

nuggets and sausages. They're just so practical!

Just fry them or toss them in the air fryer, and they're ready to enjoy with hot rice.

Especially during Ramadan, they're real lifesavers for

sahur, no need for complicated or time consuming cooking.

But yeah, not too often, though, since they're not that healthy, haha. Just once in a while is fine, and besides, they last long, so it's all good!

Maybe simple habits like this unconsciously contribute to

CMRY's profits. After all, who can resist practical nuggets and sausages for sahur or snacking?

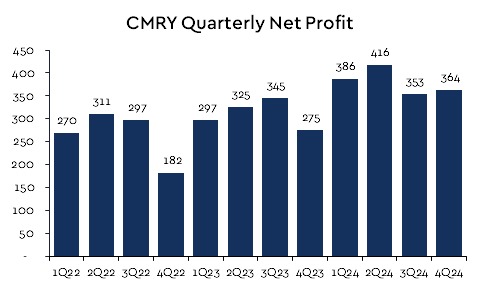

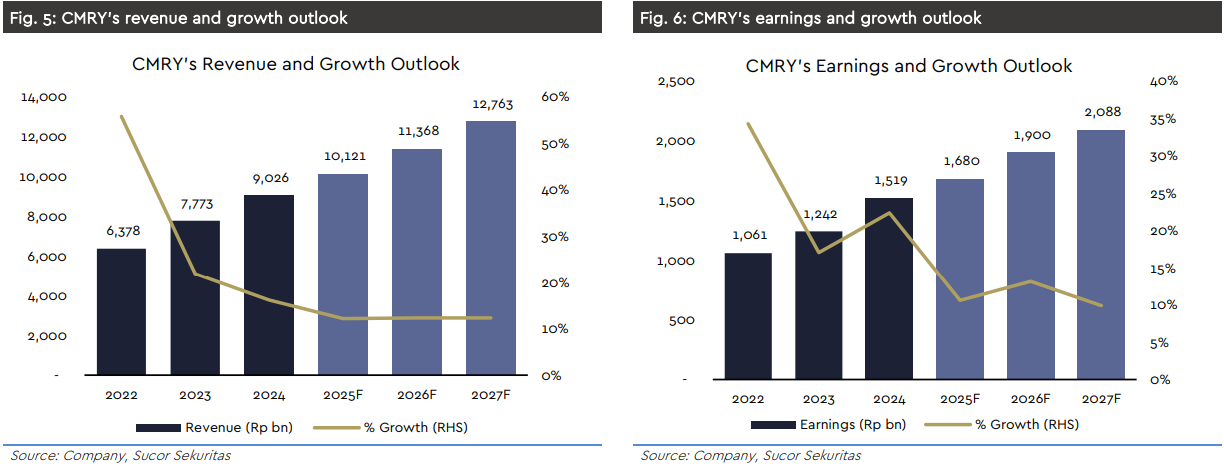

In fact, CMRY managed to book a profit of up to

IDR 1.5 tn in 2024, growing

22.4% yoy.

No wonder, really, their products have already become household staples. Plus, in the middle of all the economic drama, achieving this kind of growth is pretty impressive, right?

That big figure even managed to exceed analysts' expectations!

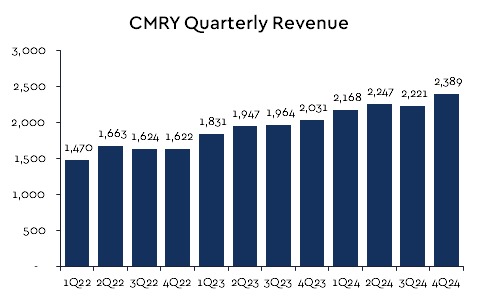

All thanks to CMRY's sales, which surged with a

16.1% yoy growth to

IDR 9.02 tn.

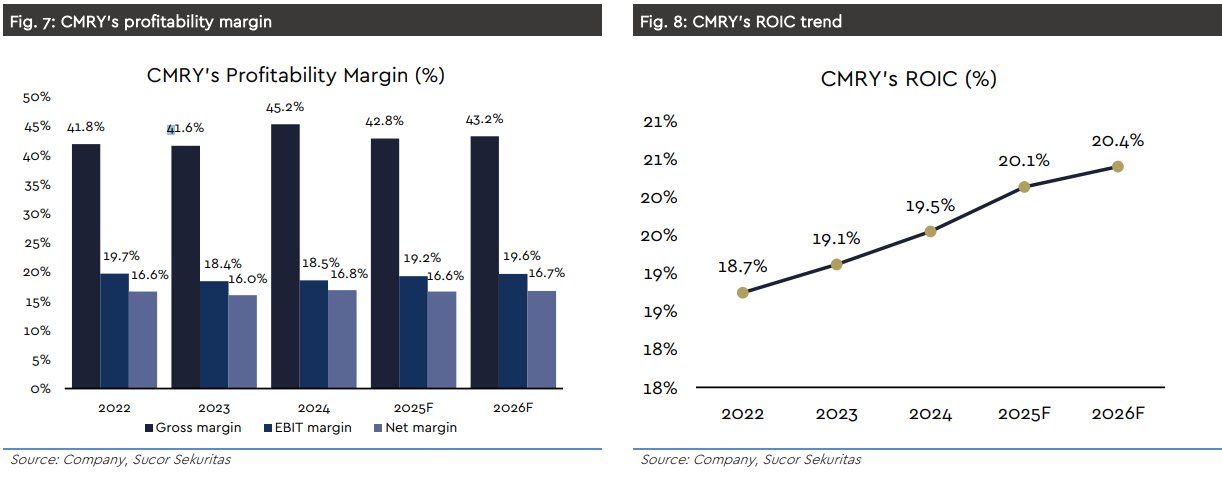

Not only that, but their

gross margin also increased to

45.2% in 2024.

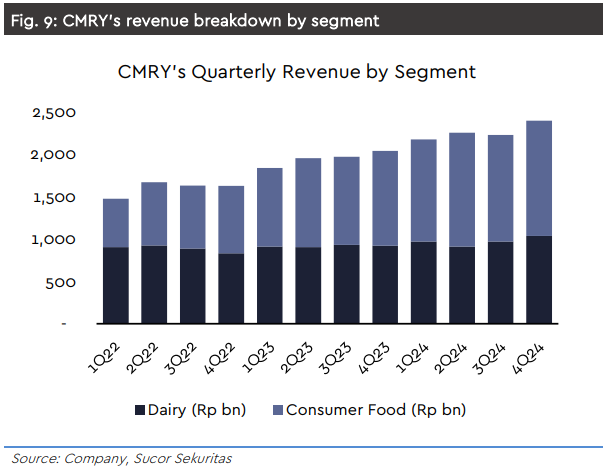

Looks like it's true, Kanzler nuggets really are one of the main contributors to CMRY's profit growth.

Turns out, revenue from the consumer foods segment, including nuggets and sausages, shot up by

25% throughout FY24!

Meanwhile, CMRY's dairy product segment only grew by

6%. Well, maybe that's because there are so many dairy product options now, making the competition tougher.

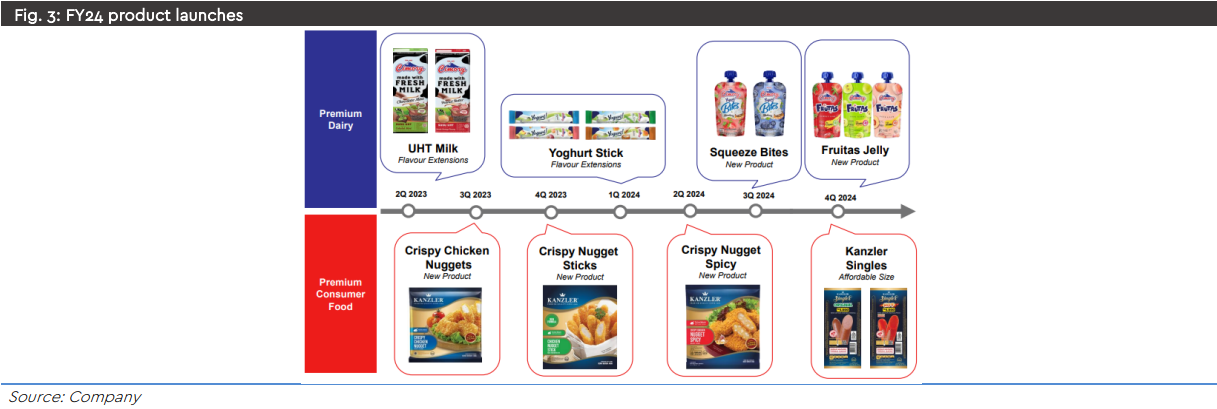

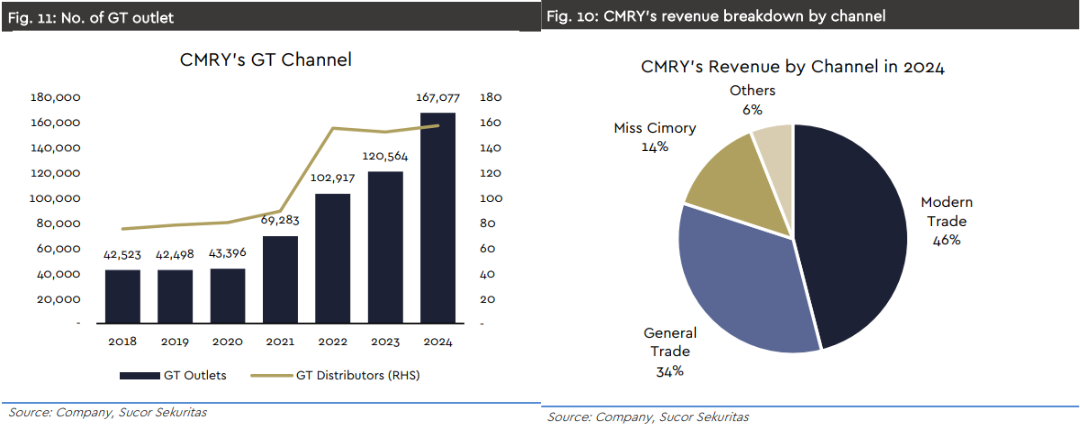

CMRY's positive performance is apparently not just thanks to nuggets and sausages but also due to successful

new product launches and a rapidly expanding sales network.

Especially in the GT channel and Miss Cimory, which are really accelerating!

Just imagine, GT outlets increased by

38% yoy, while the number of Miss Cimory agents also rose by

30% yoy.

However, for 2025, CMRY's management seems to be playing it safe. Their sales growth target is set at

10–15%, slightly lower than the previous target of

10–20%.

Gross margins are also predicted to be in the range of

42–44%. Understandable, really, since the high profitability seen in 2024 might not last long, especially if raw material prices start rising again.

Our analysts estimate that CMRY's net profit in 2025 will grow by

11% yoy to

IDR 1.68 tn.

Not only that, but they're also setting a CAGR target of

13% for the 2024–2029 period.

On the revenue side, projections indicate an increase with a CAGR of

12.3%, driven by higher sales volume.

This seems to prove that CMRY's strategy to keep pushing in the consumer foods segment and expand its network is probably the right move.

Moreover, gross margins are predicted to remain stable at

42.8% in 2025 and slightly increase to

43.2% in 2026.

Therefore, our analysts still recommend a

BUY with a target price of

IDR 5,800.

Comments