After discussing ADRO yesterday, let’s dive into its subsidiary, AADI, which is set to go public soon. Have you already subscribed via the e-IPO? How many lots did you get?

It seems allocations might be small since priority is given to ADRO shareholders who owned shares before November 26, 2024. If you’re among the lucky ones, congrats!

Why the excitement? Because AADI’s IPO looks very promising. Let’s break down why this could be a golden opportunity and explore its prospects together!

But first, a quick reminder: If you’re planning to subscribe, the subscription period is open from December 6 to December 10, 2024. Don’t miss it!

AADI is one of Indonesia's largest coal mining companies, contributing around 8% of the country’s total coal production.

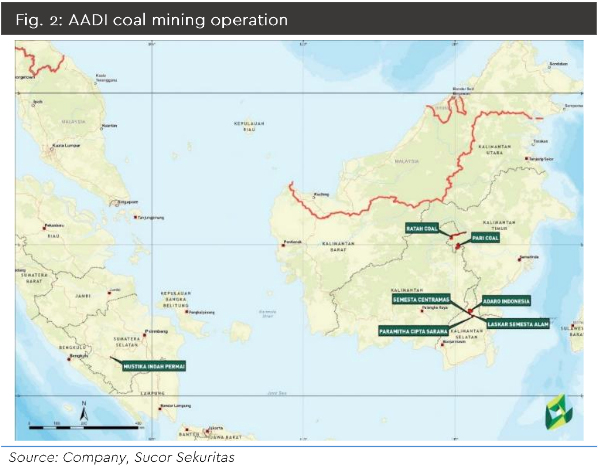

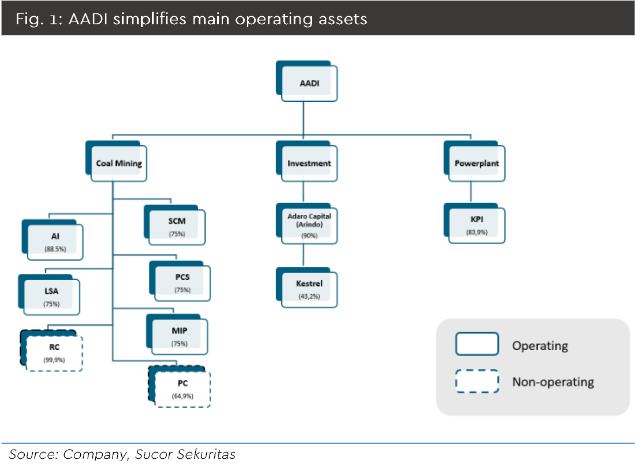

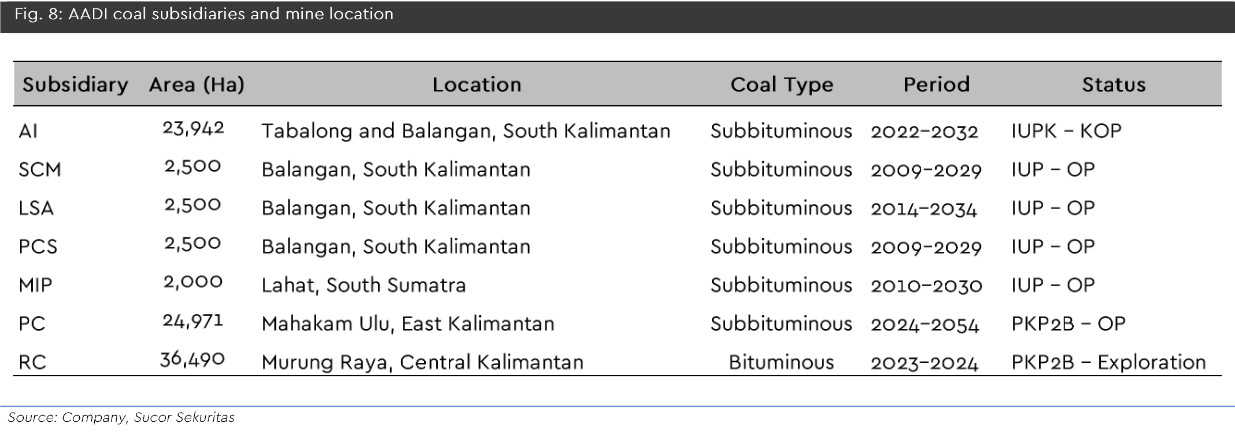

The company produces approximately 62 mn tons of coal annually and operates seven thermal coal assets, including Adaro Indonesia (AI), Laskar Semesta Alam (LSA), Semesta Centramas (SCM), Paramitha Cipta Sarana (PCS), Mustika Indah Permai (MIP), Pari Coal (PC), and Ratah Coal (RC).

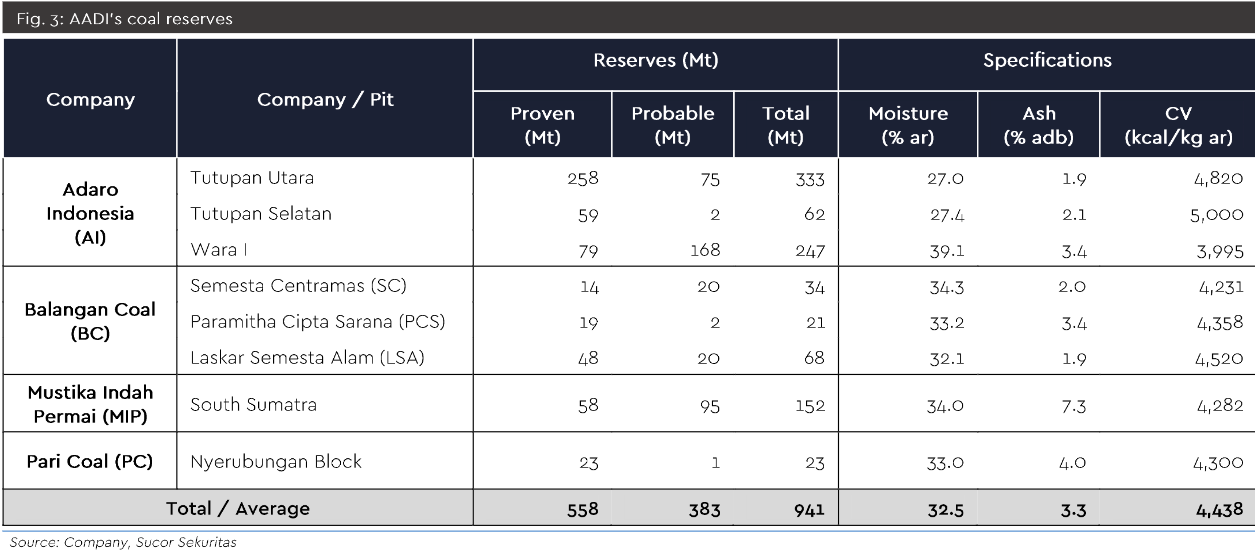

The company boasts coal reserves of 917.4 mn tons and resources of 4.1 bn tons, enough to sustain mining operations for 15 years based on reserves or up to 81 years if resources are included. This vast capacity makes AADI a compelling investment in the coal sector.

AADI also holds a 43.2% stake in the Kestrel Mine in Australia, a coking coal underground mine operated in partnership with EMR Capital.

Kestrel produced 5.6 mn tons of coal in 2023, with plans to increase output to 8 mn tons/year. The mine has 175 mn tons of reserves and 411 mn tons of resources, supporting operations for over 20 years.

In 2023, Kestrel contributed USD 50 mn to AADI’s revenue, around 5% of the total.

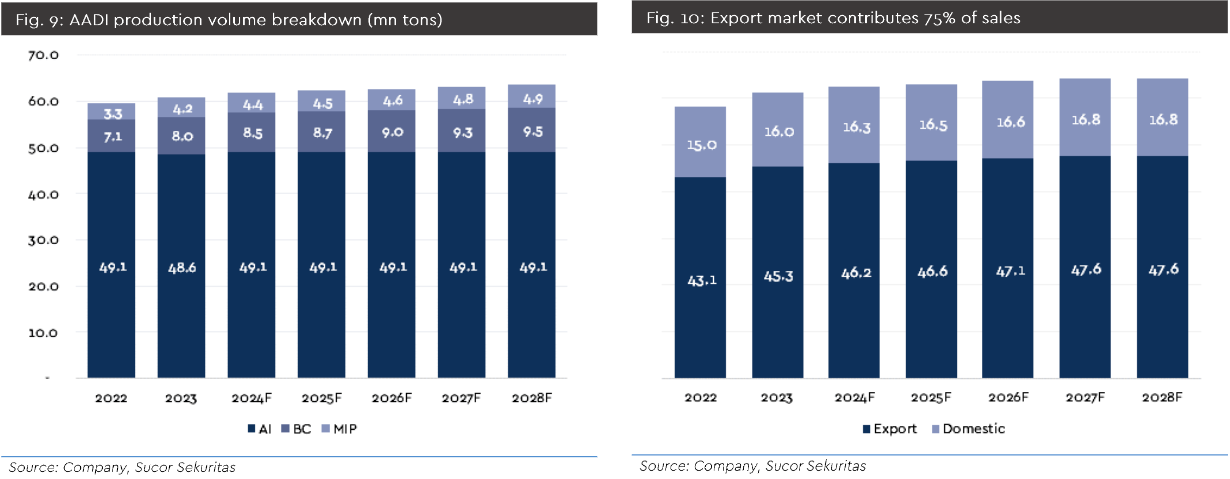

The bulk of AADI’s coal production comes from AI, which produces 49 mn tons/year, or 80% of total output. With 634 mn tons of coal reserves, AI is expected to deliver stable long-term production.

Additionally, BC and MIP, which started operations in 2014 and 2019, are projected to grow output by about

3% annually over the next five years.

Overall, AADI’s production is expected to rise from

62 mn tons in 2024 to

63.5 mn tons in 2028, driven by AI and growth from BC and MIP.

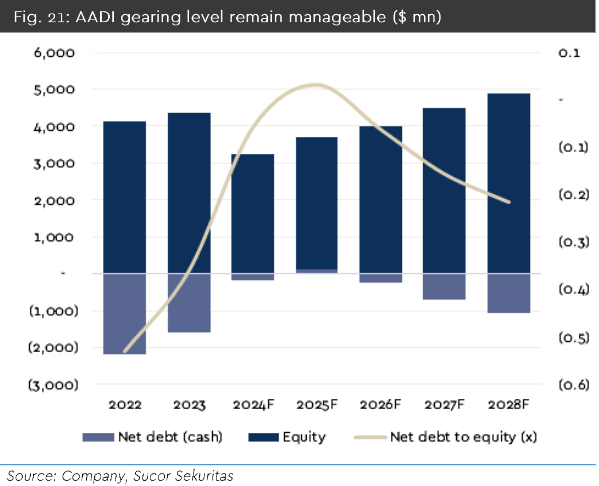

AADI is financially robust, with USD 1 bn in cash and nearly USD 1 bn in free cash flow per year. Its DER of -0.1x indicates a healthy and flexible financial position, enabling growth through internal expansion or acquisitions.

A key project in the pipeline is a 1,060 MW coal-fired power plant (CFPP), requiring USD 300 mn in capex for 2024 and USD 600 mn in 2025. Most of AADI’s capital expenditure over these two years will fund this project.

Post-2025, the company is expected to maintain USD 900 mn to USD 1 bn in free cash flow annually, providing flexibility for new projects and attractive dividend payouts.

In its first year post-IPO, AADI plans a dividend payout ratio of 45%. At the IPO price of IDR 5,550/share, the dividend yield could reach up to 20%, a very appealing figure for investors.

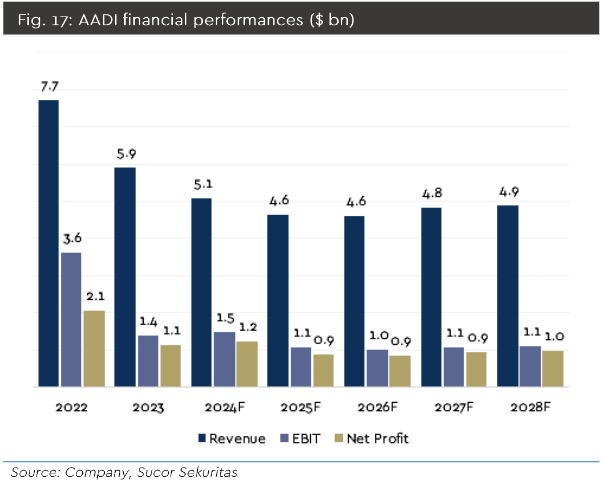

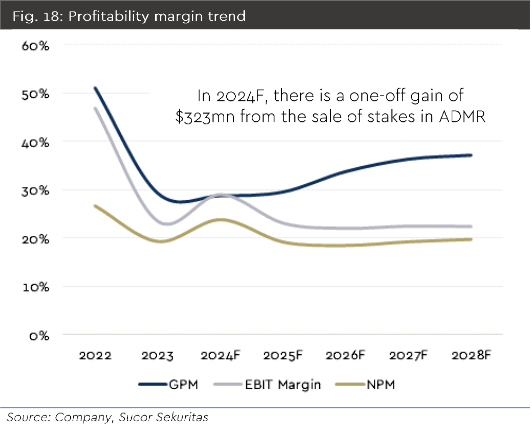

AADI’s revenue is projected to remain stable, with annual coal sales of 62-64 mn tons at an average price of USD 66/ton. This supports annual profits of approximately USD 923 mn over the next five years.

ADRO is known for achieving the highest profit margins in the coal sector due to its low production costs. A vertically integrated operation enhances supply chain efficiency, keeping costs low and profits stable, even during periods of weak coal prices.

With its solid fundamentals, strong financial position, and attractive growth potential, we recommend a BUY for AADI, with a target price of IDR 30,100.

Comments