Unilever’s stock has really been testing investors’ nerves lately.

Analysts have already issued a SELL recommendation with a low target price, yet the stock keeps dropping even further, as if it refuses to stop declining.

It’s almost like it’s saying, “You think the analysts’ target price is the lowest? Let me show you something even lower!”

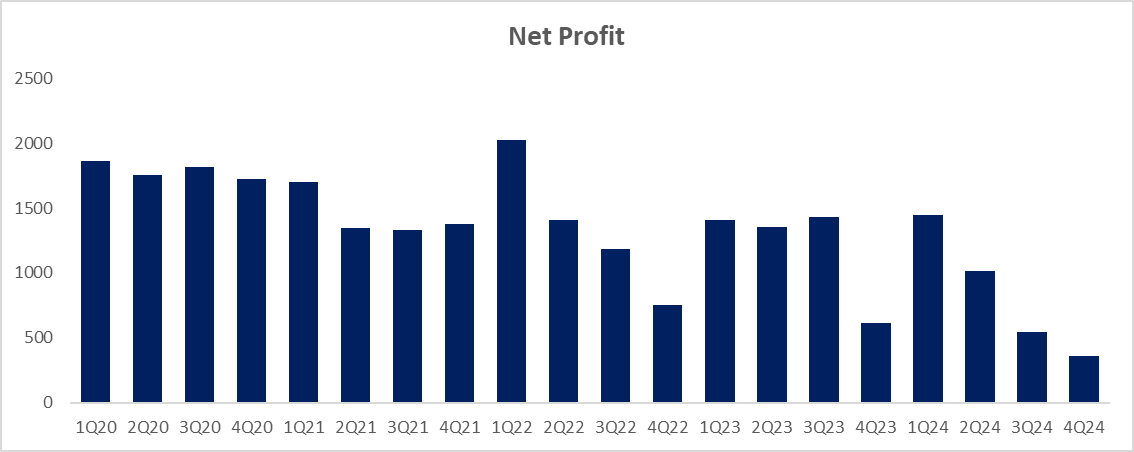

Not only is the stock price continuously falling, but so are its financial reports. UNVR just reported a 4Q24 net profit of IDR 359 bn, plunging 33.9% qoq and down 41.3% yoy.

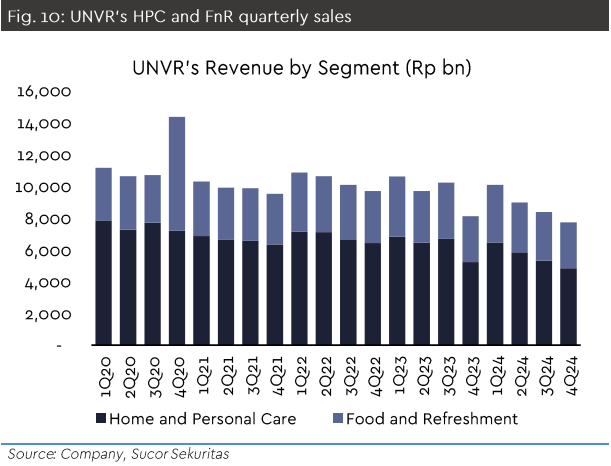

The main reason? A 2.4% yoy drop in sales volume as customers started reducing their stock levels.

It’s as if not only investors are unloading the stock, but customers are also unloading their product inventory.

By segment, sales of Home & Personal Care (HPC) products contracted by 10.8% yoy.

And yet, from what I’ve observed,

Unilever has been going all out on innovation. They’ve been actively launching new product variants, from personal care items to food products.

But apparently,

that’s still not enough to win customers back. It’s like dressing up nicely, wearing new clothes, but still getting ignored.

Management continues to blame the boycott effect, but when you think about it,

MAPI was also hit by the boycott, right?

The difference is,

MAPI has managed to bounce back, even showing solid recovery. If other brands can recover, why is Unilever still struggling?

I believe that

consumers who have left Unilever products are unlikely to return. They’ve already found alternatives that are just as good, if not cheaper.

And the competition? It’s overwhelming! From

Wings, Lion, and KAO to local brands that are now getting better at producing products on par with Unilever’s.

Nowadays, there are more choices than ever. Local brands have leveled up, offering comparable quality at more wallet-friendly prices, backed by aggressive marketing.

So it’s no surprise that people aren’t coming back to Unilever.

Maybe they’re also thinking, “Why bother using a boycotted product when there are safer alternatives that are cheaper and just as good?”

It’s a different story with MAPI. They offer something that competitors can’t easily replace.

Take Zara, for example, people will always return because they love its unique quality and design, something that’s hard to replicate.

Even if they try to find dupes elsewhere, it just doesn’t feel the same.

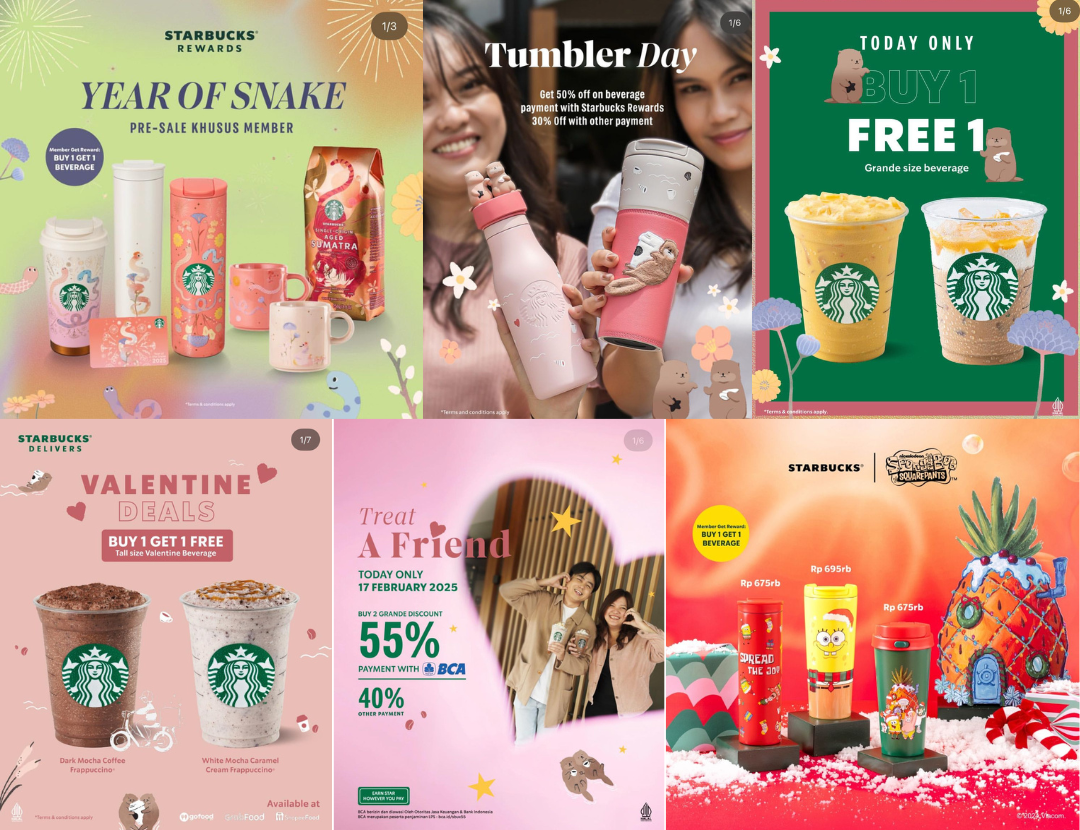

Or Starbucks. Sure, there are plenty of good local coffee options now, even cheaper ones. But still, Starbucks has a distinctive taste that’s tough to imitate.

Not to mention their irresistible promotions that keep customers coming back.

Buy 1 Get 1 deals, discounts with e-wallets, or even limited-edition tumbler collections, they know exactly how to keep customers hooked.

This is what Unilever lacks. Their products are too easily replaced, with no X-factor compelling customers to return after switching to competitors.

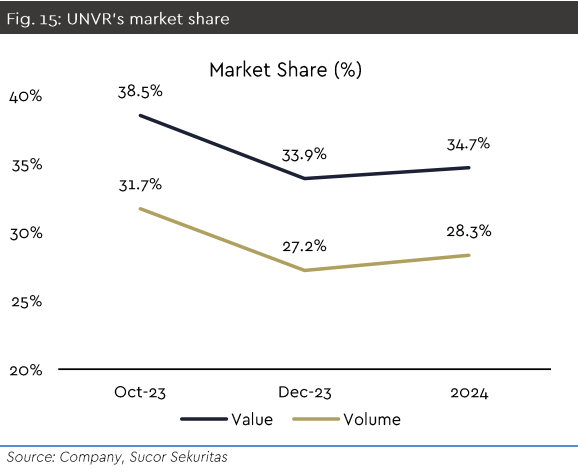

Even though UNVR’s market share volume slightly increased to 28.3% in 2024, this is still far below pre-boycott levels. So, while there’s been a bit of recovery, it’s still far from a full rebound.

To boost profits, Unilever has another strategy: divest its ice cream business for IDR 6.5 tn.

The transaction is expected to be completed in 4Q25 or 1Q26. With assets valued at around IDR 2.5 tn, they anticipate a gain of approximately IDR 3.5 tn from the sale.

So, while its core business is still struggling, at least this one-off gain can help lift the financial reports.

However, our analysts still predict weaker earnings for UNVR in 2025.

Our 2025 earnings forecast has been revised down by 14% to IDR 3.2 tn, with margins expected to remain around 9.4%-9.6%.

Only in 2026 do we project an earnings increase to IDR 5.9 tn, thanks to the profit from the ice cream divestment.

Given these conditions, we maintain our SELL recommendation for UNVR with a target price of IDR 1,260. Hopefully, it won’t drop even lower than this.

Although there’s been a slight improvement in market share and the divestment plan is set to provide a profit boost in 2026, the core business performance still shows no solid signs of recovery.

Comments