Recently, TLKM reiterated that profitability remains their top priority for 2025.

However, on the other hand, they are also playing a pricing strategy by offering a

IDR 10,000 starter pack for by.U, their secondary brand that is still trying to expand its market share.

Even though this is just a temporary strategy, we cannot ignore the fact that this move

could trigger fiercer competition.

Moreover, aggressive promotions like this are often followed by competitive responses from other players in the industry.

In the latest discussion, TLKM signaled that

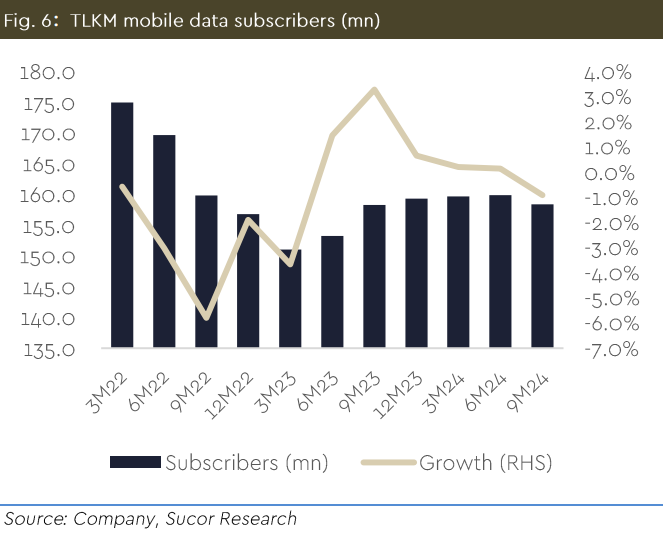

their number of subsribers continued to grow in 4Q24, even though the by.U promotion was still running and there was news about Indosat losing 4 mn subscribers.

From here, it seems that the market is starting to normalize after the

"SIM card consolidation war" that took place in mid-2024.

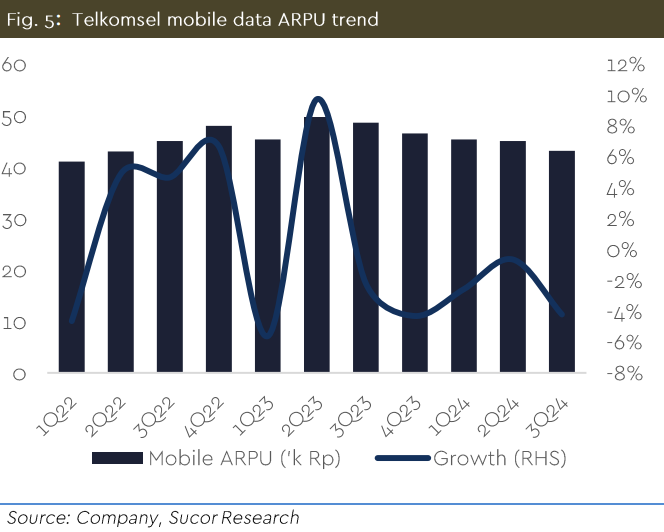

Now, regarding

ARPU, we estimate that it will remain

stable or may slightly decline qoq.

Why? Because the price adjustments made in November are likely to have little effect on 4Q24 performance, especially for long-time customers who usually take time to adapt.

So, even though TLKM’s number of customers is still growing, profitability remains a challenge if ARPU cannot increase significantly.

Increasing prices directly is not an easy option, especially if macroeconomic conditions remain sluggish and customers' purchasing power has not fully recovered.

TLKM and other players actually have several strategies to push ARPU, such as

product bundling,

converting prepaid customers to postpaid, and leveraging Fixed-Mobile Convergence synergy.

But realistically, we still have to be prepared for a conservative scenario:

ARPU has the potential to decline slightly, and the number of customers may stagnate.

We still maintain our

BUY recommendation for TLKM with a target price of

IDR 3,400, but with a note:

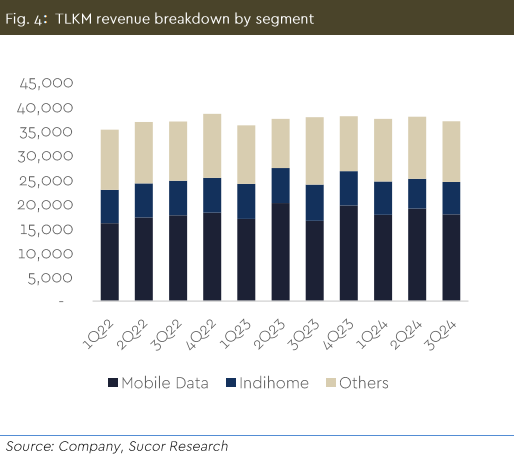

investors need to remain cautious and observe how Telkomsel will face increasingly intense competition, especially regarding ARPU from IndiHome and mobile data services.

On one hand, TLKM still has an advantage from its large scale business, but on the other hand, there are

several challenges that could make 2025 not as smooth as expected.

Competition in the data and fixed broadband segments is getting fiercer, making ARPU growth a tough challenge. Moreover, with more options available to customers, they will become

more sensitive about price and service quality.

On the other hand,

operational costs could continue to rise. If revenue does not grow as expected, profit margins could take a hit.

Not to mention, new players are starting to emerge in some areas that used to be Telkomsel’s “

stronghold.” If they can offer cheaper or more attractive services, Telkomsel’s dominance could gradually erode.

So, even though TLKM's long-term outlook remains solid, how they navigate this year will be the key.

Comments