This program caps gas prices at just

USD 6/MMBTU for seven key industrial sectors, including fertilizers, petrochemicals, oleochemicals, steel, ceramics, glass, and rubber gloves.

However, there’s still no clear indication whether the program will be extended. The Ministry of Industry has voiced its hope for

HGBT to continue, highlighting its importance in sustaining businesses and maintaining the competitiveness of domestic industries.

Without this subsidy, production costs could soar, leading to higher prices for goods. This wouldn’t just trouble businesses but would also impact consumers like us.

There’s speculation that gas subsidies for industries might be discontinued or the price could increase. If that happens, gas prices for industries like ceramics could jump to

USD 9 – USD 10/MMBTU, significantly squeezing profit margins.

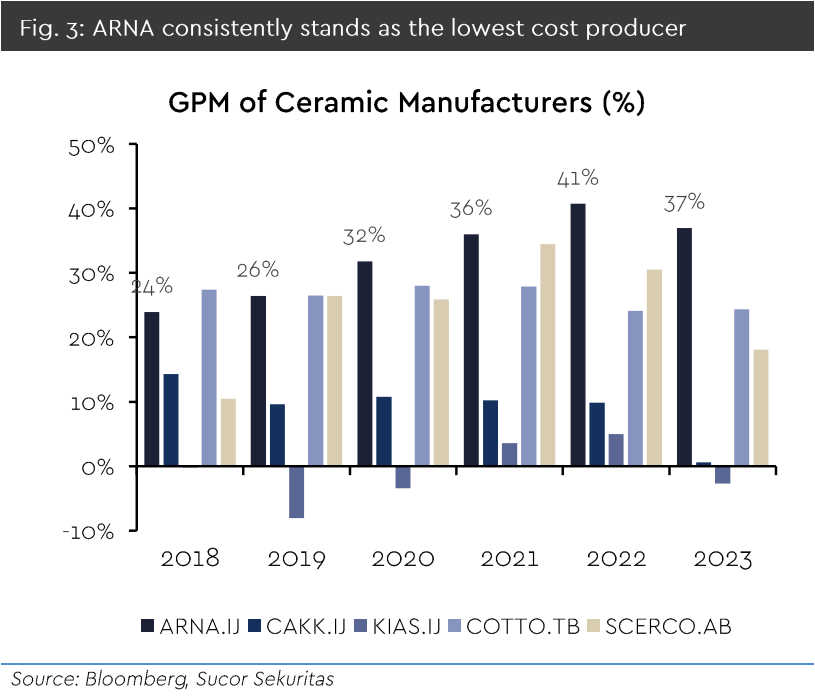

However, ceramic companies like

ARNA are in a strong position due to their low production costs compared to competitors.

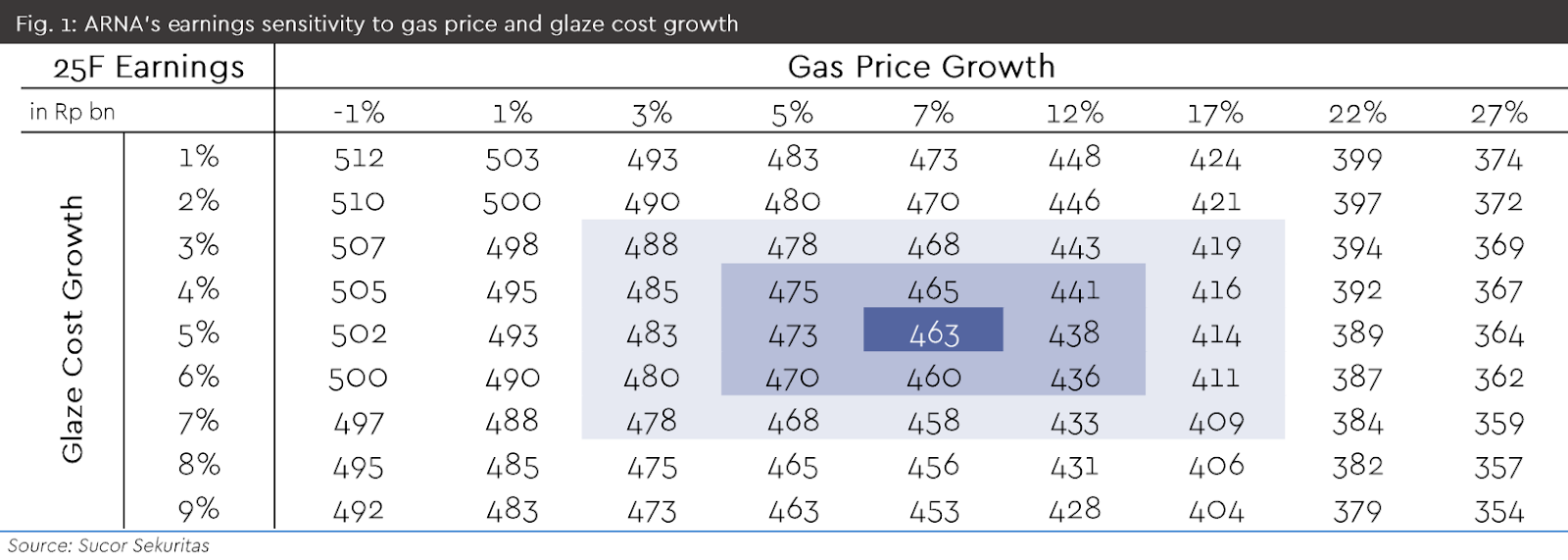

ARNA has prepared its projections for 2025. In a moderate scenario, gas prices are assumed to rise to

USD 7.5/MMBTU, coupled with a 5% annual increase in glaze costs

If this happens, ARNA’s net profit is expected to remain stable. But in a worst case scenario where gas prices hit

USD 9/MMBTU, net profit could drop by

21.3% to

IDR 364 bn.

ARNA also estimates that every

USD 1/MMBTU increase in gas prices would add around

IDR 800/sqm to production costs. This demonstrates how reliant the industry is on government policies regarding gas prices.

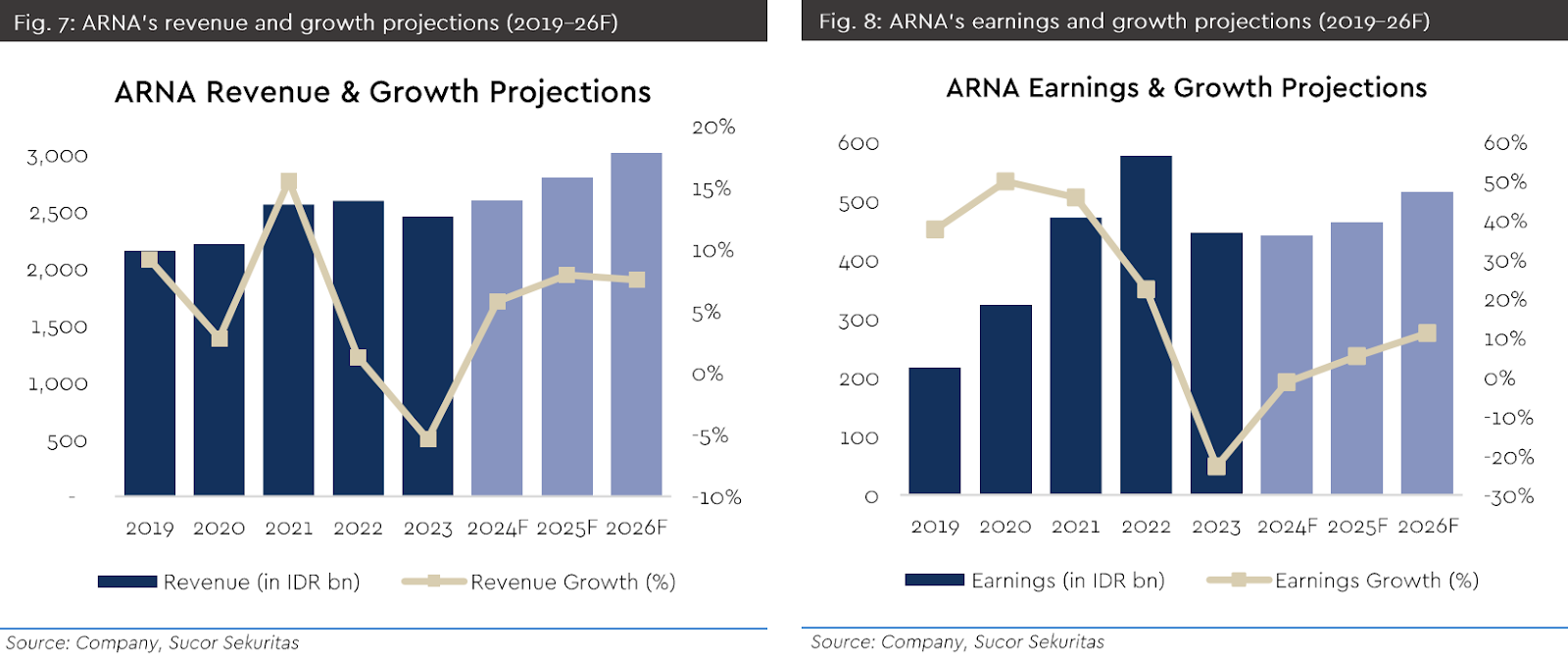

ARNA’s sales in 2Q24 are projected to grow, with volumes reaching

17.6 mn sqm, up

12% yoy.

This growth is primarily driven by higher sales volumes, supported by the new UNO Rectified production line at Plant 2, which became operational in November.

Interestingly, the growth is more volume driven, as ARNA has yet to implement significant price increases for its products. Meanwhile, importers are still clearing old stock ahead of the anti-dumping policy implementation.

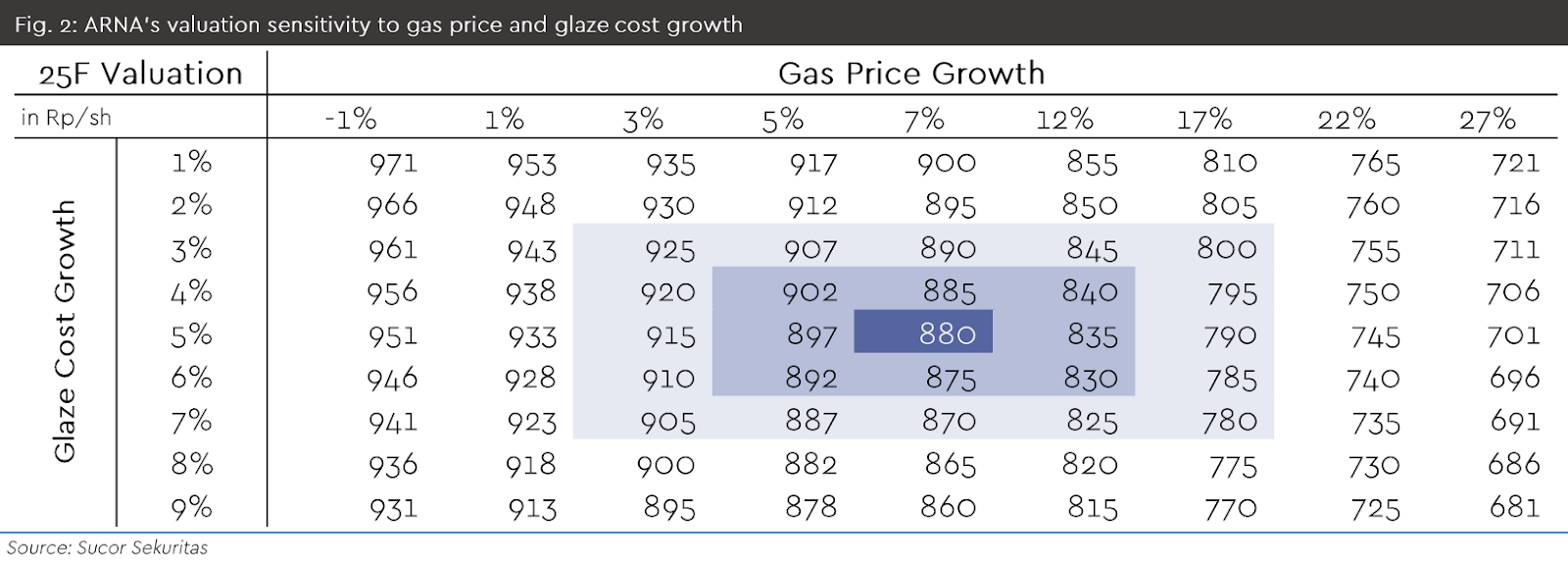

Until there is an official decision regarding the HGBT policy, we maintain a BUY recommendation for ARNA with a target price of IDR 880.

This stance is supported by plans to expand the white body plant, which will boost production capacity, as well as the anticipated full impact of Anti-Dumping Duties starting in 2025.

Additionally, we believe any gas price increases will likely be gradual rather than a sudden jump to USD 9 – USD 10/MMBTU. This gradual adjustment would help minimize the impact on ARNA’s net profit.

Comments