In 2024, one number made headlines everywhere:

IDR 271 tn! Yes, this is about the massive

tin corruption scandal that left everyone speechless.

Netizens had a field day, joking, "

If I had IDR 271 tn, what would I do with it? Haha."

So, it’s no surprise that whenever we hear about tin,

PT Timah (TINS) immediately comes to mind.

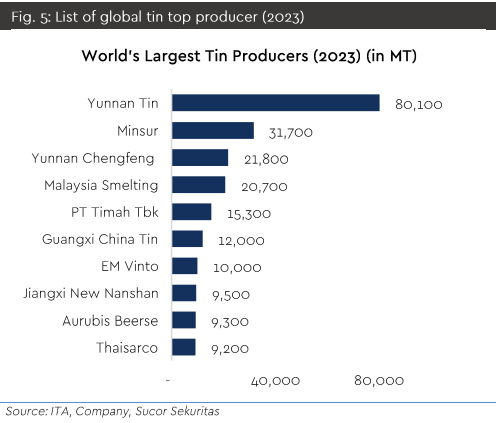

TINS is no small player. It’s the

fifth largest tin producer in the world and a key player in Indonesia's tin industry.

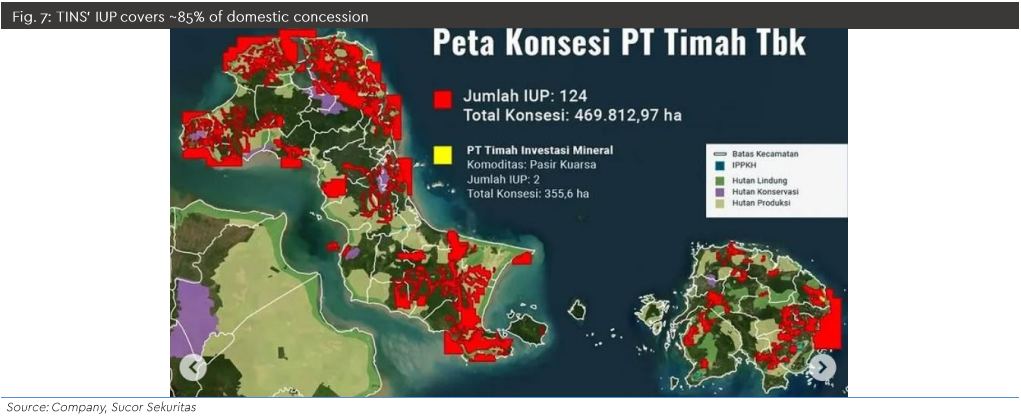

The company holds

125 mining licenses across

473.4 ha of land and sea, equivalent to

85% of all tin mining concessions in Indonesia.

Yet, despite its strong position, TINS hasn’t been performing optimally. Over the past decade, TINS’ average export share was just

40%, far behind private smelters, which claimed

60%.

In 2023, things hit rock bottom, with TINS’ export share dropping to just

18%, its lowest point in years.

The main problem is

illegal mining. Illegal miners often enter TINS’ concession areas, mine tin ore, and then sell it to private smelters at higher prices.

This leaves TINS struggling to secure enough raw materials for its own production.

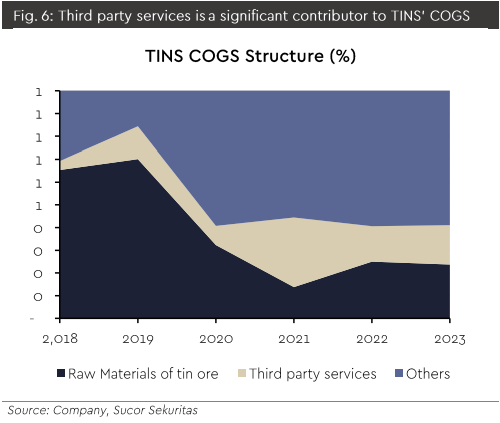

To make matters worse,

70% of TINS’ tin ore supply comes from third-party miners, while only

30% is sourced internally.

Fortunately, the government has stepped up to address these issues.

First, the government introduced new

RKAB regulations, making mining approvals more controlled: 1 year for exploration and 3 years for exploitation. Production is also limited, with only

15 RKAB approved for 2024-2026, totaling 46,400 tons. This makes it harder for illegal miners to operate.

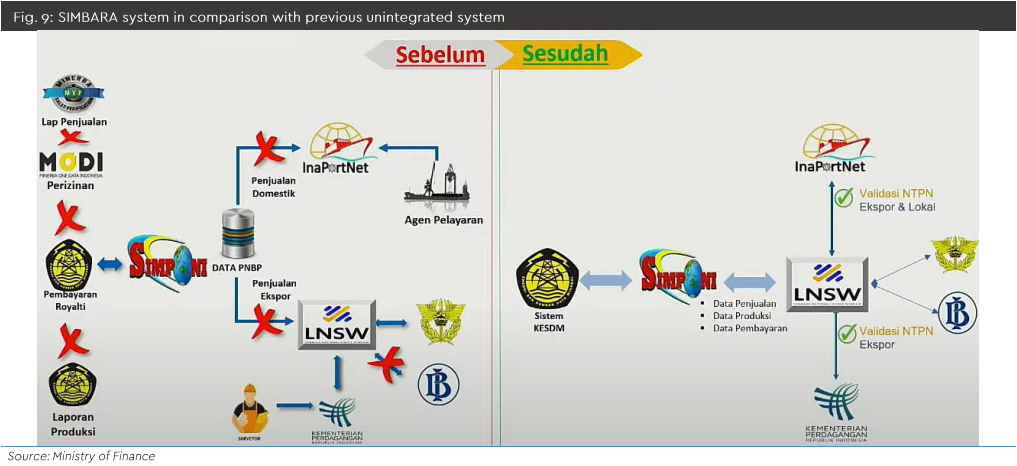

In addition, there’s also

SIMBARA, a new system tracks tin ore from mines to smelters, ensuring compliance and tax payments.

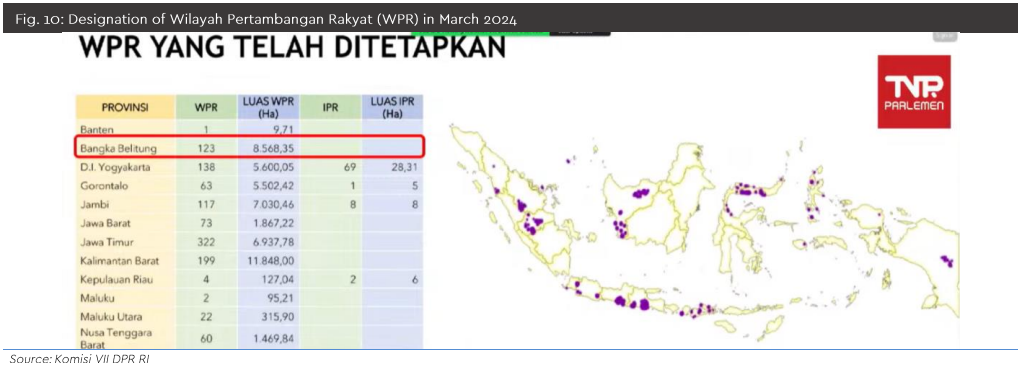

The government also created

WPR areas in Bangka Belitung covering 8,568 ha. Small scale miners must now obtain legal permits, allowing TINS to source tin outside its own concessions.

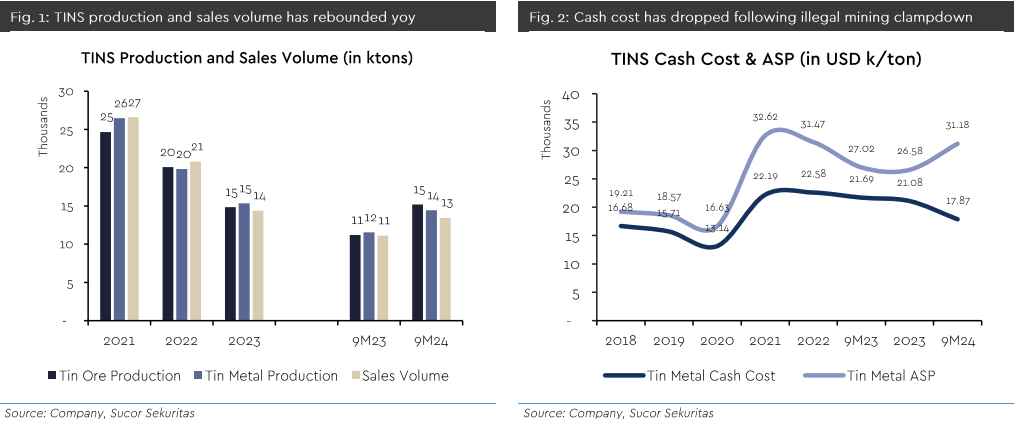

The impact is already being felt. TINS’ tin production increased significantly to

15,200 tons, up 36% yoy.

Moreover, their production costs were successfully reduced to

USD 17,800/ton, down about 18% yoy.

The government’s efforts to combat illegal mining have also been quite aggressive. Over the past year,

illegal mining has been reduced by around 37%.

Additionally,

five private smelters were shut down in early 2024, giving TINS more bargaining power. Illegal miners now have fewer buyers and are forced to sell their ore to TINS.

As a result, TINS’ export share, which had dropped to

18% in 2023, rebounded to 30% by November 2024.

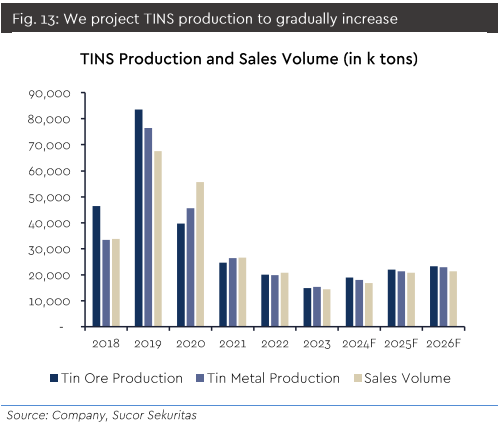

Looking ahead, TINS has big plans to increase tin metal production to

30,000 tons/year in the next few years. Their production is projected to gradually rise, starting from

21,300 tons in 2025, then to

22,900 tons in 2026.

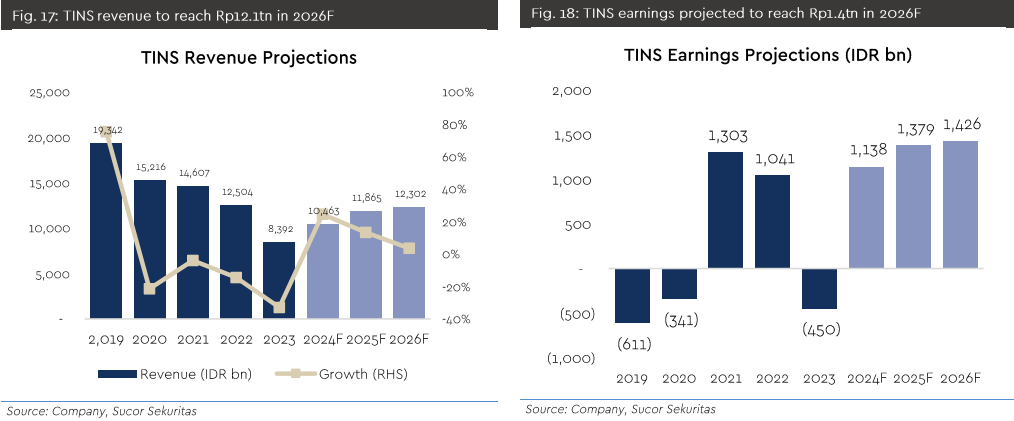

Our analysts project that TINS could record promising revenue, reaching IDR 11.8 tn in 2025 and slightly increasing to

IDR 12.1 tn in 2026. On the net profit side, the company is expected to post

IDR 1.4 tn in 2025, growing

26% yoy

With these improvements, we recommend a BUY for TINS, setting a target price of

IDR 1,740.

Comments